- [email protected]

- 07 3356 6666

- 1 Fifth Avenue, Kedron Qld 4031

Refinance Your Home Loan

Whether you’re looking to reduce your monthly commitments, tap into your property’s equity, or simply find a better product – find out whether refinancing may be right for you.

Whether your circumstances have changed, interest rates have shifted, or you’re curious about getting a better deal, refinancing your mortgage can open new doors – literally and financially.

Read our guide below to help figure out whether refinancing may be a smart option for you, then get in touch to book a no-fee refinance assessment with one of our experienced and knowledgable mortgage brokers.

What is refinancing?

Refinancing is the process of replacing your existing home, business, commercial or SMSF loan with a new one. Most refinances in Australia are to a new lender, but internal refinances are also possible.

1.

2.

What are the potential benefits of refinancing?

Reduce your repayments

Even a small reduction in your interest rate can add up to significant savings over the life of your loan.

Access equity

Refinancing can unlock the equity in your home for renovations, investments, or other personal goals, without having to sell.

Consolidate debt

Streamline multiple debts into one manageable repayment, potentially at a lower interest rate.

Pay off your home loan sooner

Reducing your interest rate and monthly repayments could potentially free up cash flow to make additional mortgage repayments and ultimately pay out your home loan sooner.

Switch to a loan (and lender) that suits you better

Your needs, priorities and financial position may have shifted since you first took out your home loan. We’ll help you discover if there’s a solution that’s more aligned with your lifestyle, goals and financial position today.

3.

Things to consider when refinancing

Refinancing comes with costs

Discharge fees, new lender setup costs, property valuations, and possible break fees (if you’re on a fixed rate) can add up. It’s essential to consult a trusted advisor to assess the cost versus savings in relation to your unique situation.

Your financial position and loan eligibility may have changed

If your income, expenses, employment, or credit score has changed, you may not qualify for the best rates or be able to refinance at all. It’s essential to disclose any changes with your mortgage adviser upfront, as it guides lender and product selection. Failing to provide all relevant information could result in a bank declining your loan application and an unnecessary hit on your credit score.

It’s also important to note that government and bank policies can change at any time to suit economic conditions. This can result in tightening of lending policy so that whilst an applicant’s position may not have changed, they may be able to borrow less than they could, say a year ago.

Property Value and Loan-to-Value Ratio (LVR)

If your loan-to-value ratio (LVR) is too high, you might be stuck paying Lenders Mortgage Insurance (LMI) again or be ineligible to switch. Your LVR may be too high if you haven’t yet paid down a sufficient portion of the initial principal amount borrowed, or if the value of your property has decreased.

Alternatively, if your property has significantly increased in value since you took out your existing loan, you may be able to refinance sooner than expected.

Loan Features and Ongoing Costs

Consider the loan features you want moving forward, such as multiple offset accounts, redraw facilities, the ability to make additional repayments, and the ability to switch between fixed and variable interest rates. Sometimes, additional loan features come with recurring monthly or annual fees, which you should be aware of prior to switching.

You could reset the loan term

Extending your loan term back out to 30 years could mean paying more interest over time, even if your monthly repayments drop. Let us know whether or not you want to reset the term, and we’ll run the figures to determine if it works and whether it’s a smart move for your long term plans.

Time and effort involved

There’s paperwork and processing time involved, even with broker support. Get clear on your goals before starting the process, and we’ll do our best to make it as easy for you as possible.

Removing a loan guarantor

It’s increasingly common for first home buyers to use ‘the bank of mum and dad’ to enter the property market. If you have a family guarantee on your mortgage and you are not in a strong enough equity position to remove the guarantor, refinancing may not be right at the moment.

Alternatively, you may wish to refinance to a new lender and product, such as a 90% no LMI loan to gain independence by removing the guarantor.

Seek professional advice

There are dozens of lenders in Australia and hundreds of mortgage products available, each with their own features, intricacies and policy niches. Whilst your friend may tell you how great their home loan product, or experience with a particular lender is, it’s not necessarily the right fit for you.

At Aspire, we have a wealth of lending knowledge and experience, and a vast panel of lenders and products to choose from. We’ll provide you with honest information upfront and help you find a smart path forward.

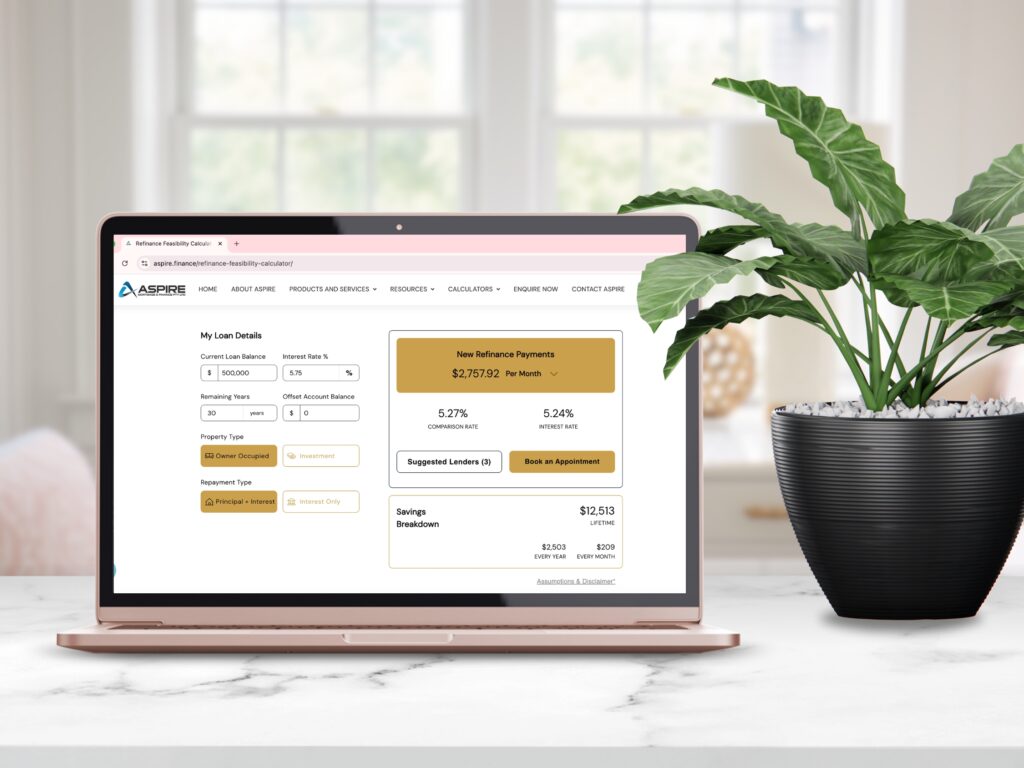

Thinking about refinancing but not sure if it stacks up?

Use our quick and easy Refinance Feasibility Calculator to see how much you could save.

Other useful resources:

Ready to explore your options?

Refinancing isn’t just about getting a better rate, it’s about making your mortgage work harder for you.

Book a no-obligation chat with our team today and explore what refinancing could mean for your future.